Retirement Planning

Jeremy Ko

Ph.D.

How Married Couples Can Optimize Their Social Security Retirement Benefits

Timing your Social Security claims as a married couple can significantly increase your lifetime benefits. Discover strategies based on expected lifespan and relative earnings.

A key question that retirees can face is when to claim their Social Security benefits. Social Security retirement benefits can offer an important source of retirement funding as they currently provide up to approximately $62,000 per year per individual in lifetime income, which grows with the cost of living. Personal retirement benefits (based on your own work record) can be claimed as early as age 62, and max out at age 70. Claiming at earlier ages provides payments that start earlier but are lower per month. Claiming at later ages provides payments that start later but are higher per month.

While this decision might feel overwhelming—especially for married couples whose claiming decisions can interact—understanding a few key factors can help you approach it with confidence. One critical input to the claiming decision is expected lifespan. Someone with a long expected lifespan should typically claim late because they expect many monthly payments over the course of their life. Someone with a short expected lifespan should typically claim early to not miss out on payments in their early to mid-60s. Higher monthly payments from delayed Social Security claiming make a bigger difference to someone expecting more monthly payments during a longer lifespan. For example, $100 additional dollars per month equals $36,000 more over a lifetime for someone expecting 360 monthly payments over their remaining life (of 30 years). It only equals $12,000 more for someone expecting 120 monthly payments over their remaining life (of 10 years). This Social Security calculator for singles provides information about the value of claiming at different ages based on expected lifespan.

Understanding spousal and survivor Social Security benefits

The situation can get more complicated for a married couple who might also consider spousal and survivor benefits, which allow one spouse to earn benefits based on the other's work record. Spousal benefits can be claimed as early as age 62. Survivor benefits, which can become available if one spouse is deceased, can be claimed as early as age 60. Both types of benefits max out at full retirement age, which is currently age 67 (for anyone born after Jan 1, 1962).

It is important to note that you can earn only one benefit at a time. Individuals who qualify for both a personal and spousal benefit can only earn the higher of the two. This is where strategic planning becomes essential for married couples.

A thoughtful approach to timing can significantly increase your lifetime benefits. There are a variety of factors that should be considered when deciding when to claim Social Security benefits including your resources and needs, employment, taxes, effects on other benefits (e.g., Medicare premiums), etc. This blog post provides a few simplified strategies that you might consider if you're married based on two important factors: expected lifespan and the relative earnings of the two spouses.

Defining one earner and two earner couples

For illustrative purposes, I categorize couples as "one earner" and "two earner," as described below:

Two earner couple: Each member's personal benefit is either roughly equal to or greater than their spousal benefit. This can happen when both spouses have similar "average" earnings over time (as computed by Social Security).

One earner couple: One member's spousal benefit (based on their spouse's earnings) is substantially higher than their personal benefit (based on their own work record). In this instance, one spouse typically earned much less than their spouse over their working years or worked many fewer years and will collect their spousal and survivor benefits (and not their personal benefit) in retirement.

You can estimate benefits for yourself and your spouse on the Social Security Administration Plan for Retirement website. These estimates can tell you whether you might be part of a one earner or two earner couple.

Considering expected lifespan in your Social Security claiming strategy

I also consider couples where both spouses have either shorter or longer expected lifespans relative to the US median lifespan of 85 or 88 years old for males and females, respectively, who are currently 62 years old. You can also consider the long lifespan case if you want to be conservative in your retirement income planning. This approach can help ensure that you have adequate income even if you and your spouse live beyond your expected lifespans into old age. Taking a conservative approach gives you peace of mind that your financial security won't run out, even if you're fortunate enough to enjoy many years in retirement.

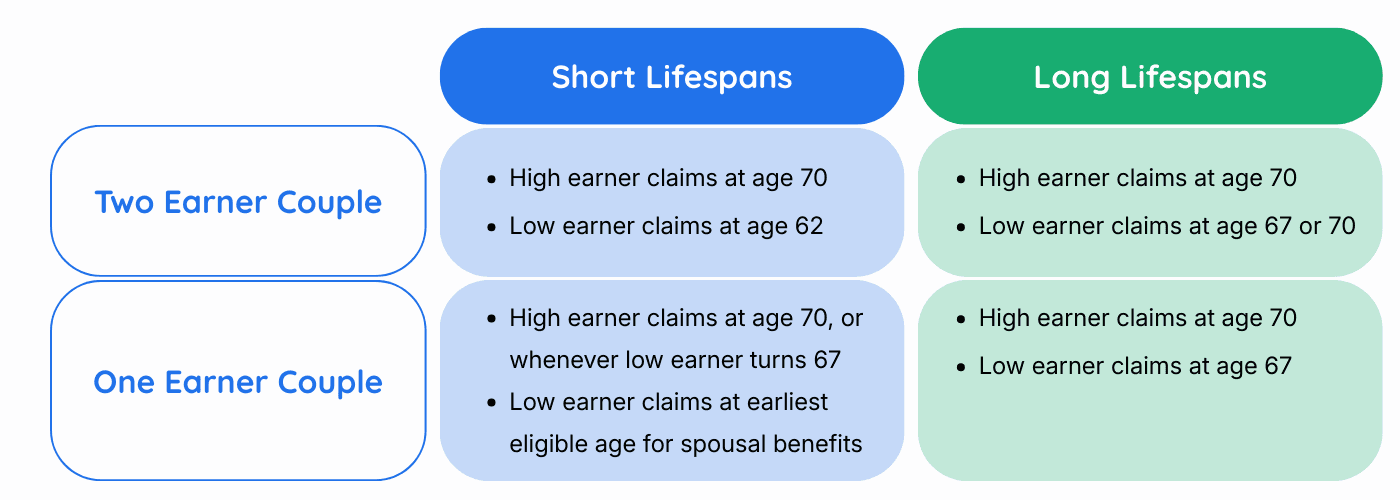

Strategic claiming approaches for four couple types

The table below shows claiming strategies for the four types of couples: two earner couples with short or long lifespans and one earner couples with short or long lifespans. In this analysis, the "high earner" is the spouse with the higher personal benefit at full retirement age as reported by SSA. The "low earner" is the spouse with the lower personal benefit.

Generally speaking, the high earner should claim late at age 70, as the high earner's benefit is typically passed on to the low earner in the form of a survivor benefit when the high earner dies. Hence, the high earner's monthly benefit should generally be maximized because it can last a long time. The only exception to this rule is the case of a one earner couple with short lifespans, and I explain why things differ in this case below.

Having a framework helps simplify what might otherwise feel like an overwhelming number of scenarios, so let's now get into the details of why the strategies listed below can work well in these four cases.

Two earner couples with short lifespans

The high earner generally wants to maximize their monthly benefit by claiming at age 70. As mentioned, the higher earner's benefit is typically long-lived because it can be passed along as a survivor benefit to the low earner. The low earner claims early at age 62 because their benefit is generally short-lived. The low earner will switch from their personal benefit to their survivor benefit if their spouse dies first. Otherwise, their benefit disappears if the low earner dies first. Short-lived benefits should be claimed early because otherwise the claimant misses out on benefits in their early to mid-60s.

Two earner couples with long lifespans

Both the high earner's benefit and the low earner's benefit are expected to last a long time because both spouses are expected to have long lifespans. Therefore, the high earner wants to maximize their benefit by claiming at age 70. The low earner also wants to maximize their benefit by claiming late. There are two possible cases for the low earner. The first case is when the low earner has a higher spousal benefit than their personal benefit. In this case, the low earner claims at age 67, when monthly spousal benefits max out. The second case is when the low earner has a higher personal benefit than their spousal benefit. In this case, the low earner claims at age 70, when personal benefits max out.

One earner couples with short lifespans

The high earner, in principle, still wants to max out their benefit by claiming at age 70 in this case. However, the higher earner now has an additional consideration. That is, the low earner is relying on spousal benefits in retirement and is not eligible for them until the high earner claims. These spousal benefits max out when the low earner turns 67. Therefore, the high earner does not want to wait beyond the low earner's 67th birthday to claim.

The high earner should claim at age 70 if the low earner hasn't turned 67 by then. Otherwise, the high earner should claim whenever the low earner turns 67 so the couple doesn't miss out on any spousal benefits once they max out. The low earner has a short-lived benefit so they want to claim as soon as they are eligible, i.e., when the low earner turns 62 or whenever the higher earner claims (whichever comes later).

For example, a high earner that is five years older should claim at 70, while the low earner claims at their earliest eligible age of 65. Alternatively, a high earner that is five years younger should not wait until age 70 to claim since their spouse will be age 75 at this point. The high earner should instead claim at age 62 to enable the low earner to claim at age 67.

One earner couples with long lifespans

Again, both the high earner's benefit and the low earner's benefit are expected to last a long time in this case. Therefore, the high earner wants to maximize their benefit by claiming at age 70. The low earner also wants to maximize their benefit by claiming at age 67 when their spousal benefits max out.

Getting professional help with your Social Security decision

Please understand that the rules-of-thumb above represent a starting point when a couple thinks about when to claim Social Security benefits. Every couple's situation is unique, and what works for one may not be optimal for another. You may want to consult a financial professional when making such a complex decision with potentially big implications for your financial well-being in retirement.

If you’re not sure where to start, you can book a 20-minute or 50-minute session with a Mentor in your Fruition app. Taking the time to understand your options now can lead to significantly better financial outcomes throughout your retirement years.