Retirement Planning

Jeremy Ko

Ph.D.

What You Need to Know About Social Security Benefits in Retirement

Ever wondered how Social Security actually works? Understanding the three types of retirement benefits—personal, spousal, and survivor—could help you maximize your monthly income in retirement.

Social security benefits represent a big chunk of retirement income for the vast majority of US households. As of 2025, retirement benefits can provide up to around $5000 per month (or $60,000 per year) for a retiree, which adds up to around $670,000 of value over a typical lifespan! I’ve personally seen how social security benefits can make a BIG difference in people’s well-being in retirement. So it’s important to know about the types of social security benefits and how they work.

What are the different types of Social Security Benefits?

I’m going to help you understand three types of social security benefits for people in or near retirement: personal, spousal, and survivor benefits.¹ The amount of these benefits is based on earnings history and the age at which they are claimed. Before we jump into it, there are two important things to know upfront:

Claiming at earlier ages gives you payments which start earlier but are lower per month. Claiming at later ages gives you payments that start later but are higher per month.

You can only earn one type of benefit at a time! If you’re eligible for both a personal and spousal benefit, you can only earn the higher of the two – not both. Alternatively, suppose you’re earning a personal benefit and your spouse passes away. If you were to claim a survivor benefit, you would then lose your personal benefit if it is lower.

The exact rules behind social security retirement benefits are complicated, but here are some basics about each type that you should know.

Personal retirement benefits

Personal benefits are based on a person's earnings history. To be specific, they are based on the average a person's highest 35 years of "indexed" earnings. Indexed means that past earnings are inflated to reflect the fact that wages have grown over time.² The earnings in this average are also capped at a maximum amount – which is currently $176,000 per year in 2025. You need to have worked for at least ten years to be eligible for personal benefits.

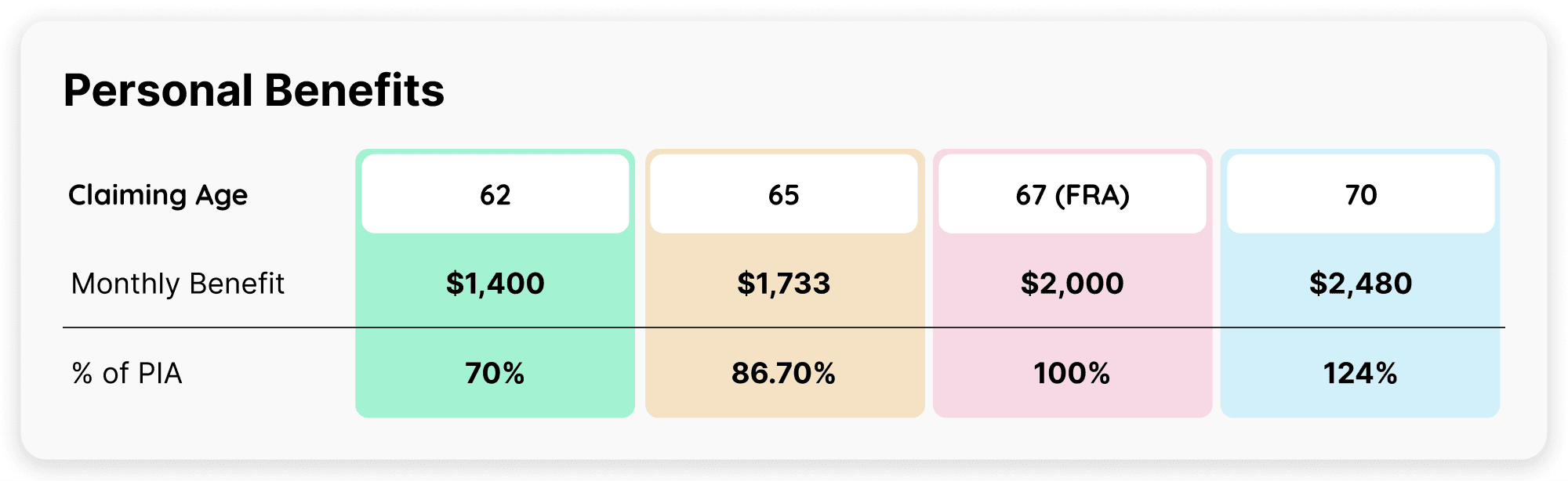

Personal benefits can be claimed anytime starting at age 62, and they max out at age 70. The following table shows the amount of personal benefit you'd earn for four different claiming ages. The table assumes your primary insurance amount (PIA) to be $2000 per month. Your PIA is your monthly benefit if you claim at your full retirement age (FRA) – which is 67 for anyone born in 1960 or later. You would earn $1400 per month in "real" terms (i.e., in terms of spending power) if you were to claim at age 62. In contrast, you would earn much more – $2480 per month – if you were to claim at age 70. You can find more information about personal retirement benefits here.

Spousal retirement benefits

Spousal benefits are based on your spouse's PIA. They can be claimed anytime starting at age 62, and they max out at your FRA (i.e., age 67 for anyone born in 1960 or later). Spouses may also receive benefits before age 62 if they have dependent children.

Generally, individuals can earn spousal benefits if married for more than one year. Divorced individuals can earn spousal benefits based on their ex-spouse's PIA if married for more than ten years and currently unmarried.

You can only earn spousal benefits once your spouse has claimed his/her personal benefit. However, there is an exception for some divorcees!

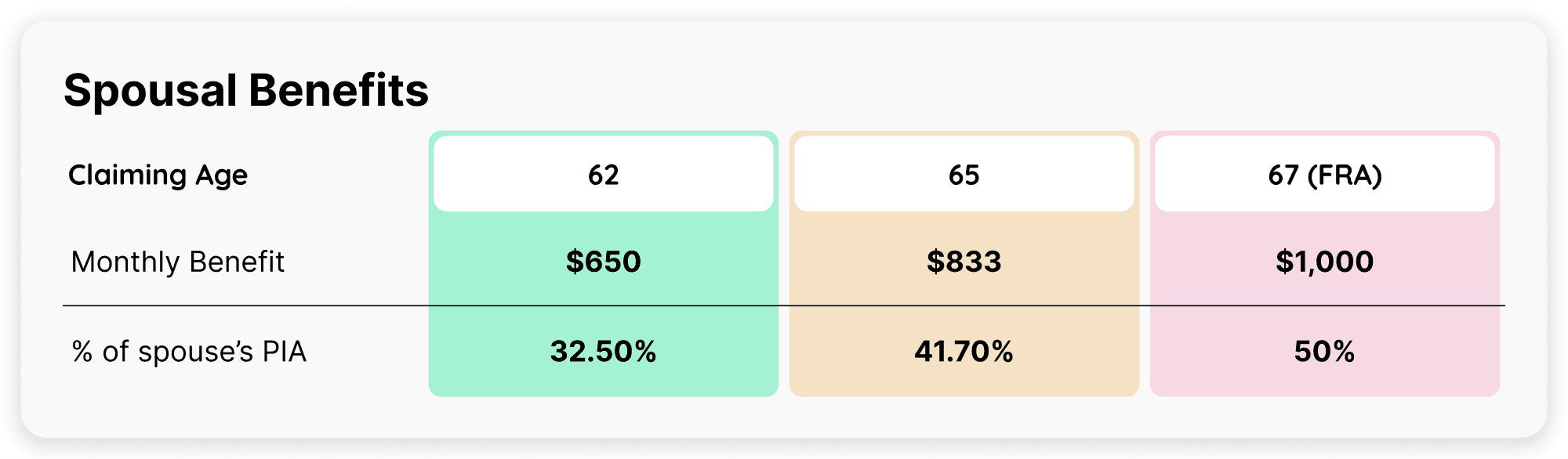

The following table shows the amount of spousal benefit you'd earn for three different claiming ages – assuming that your spouse has a PIA of $2000 and has already claimed. You could earn up to $1000 per month or 50% of that PIA. You would only earn $650 per month or 32.5% of your spouse's PIA if you were to claim at age 62. You can find more detailed information here.

Survivor benefits

You may be eligible for survivor benefits on your spouse's earnings history after they pass away. Your survivor benefit is based not on your spouse's PIA but rather on the benefit they were earning or were eligible for at the time of their death – subject to a minimum benefit.

Survivor benefits can be claimed (once a spouse dies) anytime starting at age 60 for the surviving spouse, and they max out at the survivor's FRA. Please note that the full retirement age for survivor benefits is different from that for personal and spousal benefits. It is age 67 for anyone born after January 1, 1962.

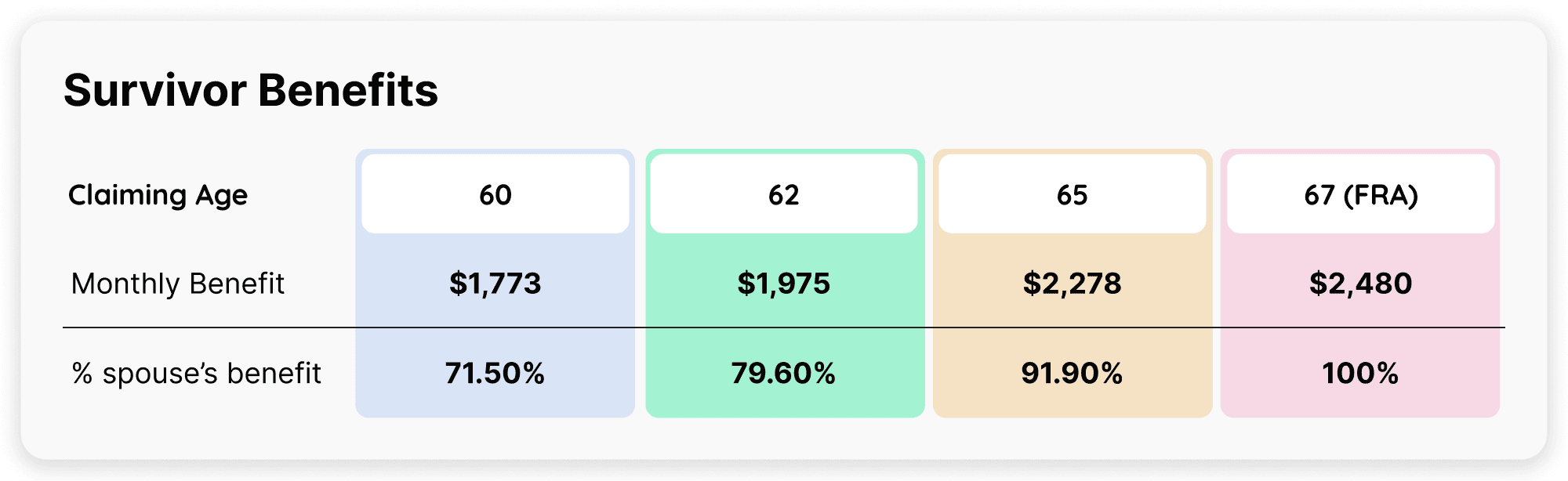

The following table shows the amount of survivor benefit you'd earn for four different claiming ages. This table assumes that your spouse (with PIA of $2000) claimed at age 70 before passing away. Therefore, they were earning $2480 per month before their death. You'd only earn $1773 per month (or 71.5% of your spouse's benefit) if you were to claim at age 60. You'd earn the full amount of this benefit – all $2480 per month – if you were to defer claiming until your FRA.

Therefore, a spouse can pass along their benefit to their surviving spouse upon their death! As a result, it often makes sense for the primary earner in a couple (i.e., the spouse with the higher PIA) to claim as late as possible so that their monthly benefit is as high as possible.

Surviving spouses may be eligible for survivor benefits before age 60 if they have dependent children or are disabled. Dependent children and parents may also be eligible for their own separate survivor benefits. You can find more detailed information regarding survivor benefits here.

Other important considerations

There are at least two more basic things to know about social security retirement and survivor benefits:

Penalties

There are possible penalties on social security benefits when earning income from work prior to FRA. Total income within certain categories that is above a specific limit (currently $23,400 in 2025) results in a reduction in your social security benefit, which is paid back after FRA. You can work as much as you want after FRA without penalty.

Inflation

Social security benefits are indexed to inflation. In other words, they increase with the cost of living over time. Hence, suppose you had PIA of $2000 at your FRA of age 67. You would earn not only $2480 per month when claiming at age 70, but also any increases in the cost of living from age 67 to 70.

Parting thoughts

I know how complicated these details about personal, spousal, and survivor benefits can be. We have hit the core concepts related to these benefits, but there are still other complications that we haven’t covered. You may benefit from further research or a consultation with a financial professional.

Please keep in mind that social security benefits are an important piece of the retirement security puzzle! Choosing when to claim deserves careful thought and consideration of relevant factors such as financial needs, lifespan, taxes, work penalties, etc. You can find a free online social security calculator, like this one from ShoreUp Retirement Solutions, which provides information about the value of claiming at different ages, focusing on lifespan considerations.

¹Social security also offers disability benefits, which we do not discuss here. ²Suppose you earned $50,000 back in 1990. This amount would be inflated forward to 2025 to approximately $160,000 (which would then count toward your average indexed earnings), as earnings in the US have increased by over three times since 1990.

About the author

Jeremy Ko

Ph.D.

K. Jeremy Ko has been working in the area of financial education, planning, and research for over twenty years. He has focused on retirement and social security planning for almost 15 of those years. He has a passion for helping people achieve lifelong financial security. His educational and professional credentials include a PhD in financial economics from the MIT Sloan School of Management, an academic teaching/research position in the finance department of Penn State’s Smeal School of Business, and a leadership position at a top-ranked independent financial advisory firm - Edelman Financial Engines.