Debt Management

Gilles Hudelot

AFC®, CFP®, CRPS®

Snowballs vs Avalanches: Which Debt Paydown Strategy is Right for You?

With average household debt at $105K, smart strategies can help. The Snowball Method targets smallest balances first, building momentum as you pay off debts one by one.

Do you ever feel overwhelmed by debt? You are not alone.

The average American household has $105,056 of debt as of the end of 2024. 30% of that is non-housing debt (Auto Loan, Credit Card, Student Loan, and other personal and medical debt). Credit card debt also increased by 4% since last year, with an average balance of $6,380.

These figures may seem overwhelming, but there are smart ways to work on paying down your debts. We’ll review strategies that may work for you.

Finding the right method for you

Let’s start by gathering information about your situation. You’ll need the following:

Name of Credit Card or Debt

Amount owed

Interest rate you are paying

Minimum Payment

Special information, like if the interest rate will increase or if there is a balloon payment

Next, let’s review your budget and determine an additional amount we want to allocate monthly to pay down our debts more quickly. The amount should be something we can handle consistently each month. We can always choose to add a little extra month to month. We’ll call it your snowball.

We will continue to pay the minimum required each month to ensure our payments stay on track, but we will also add extra payments to one debt at a time. The debt we choose will depend on the strategy we focus on.

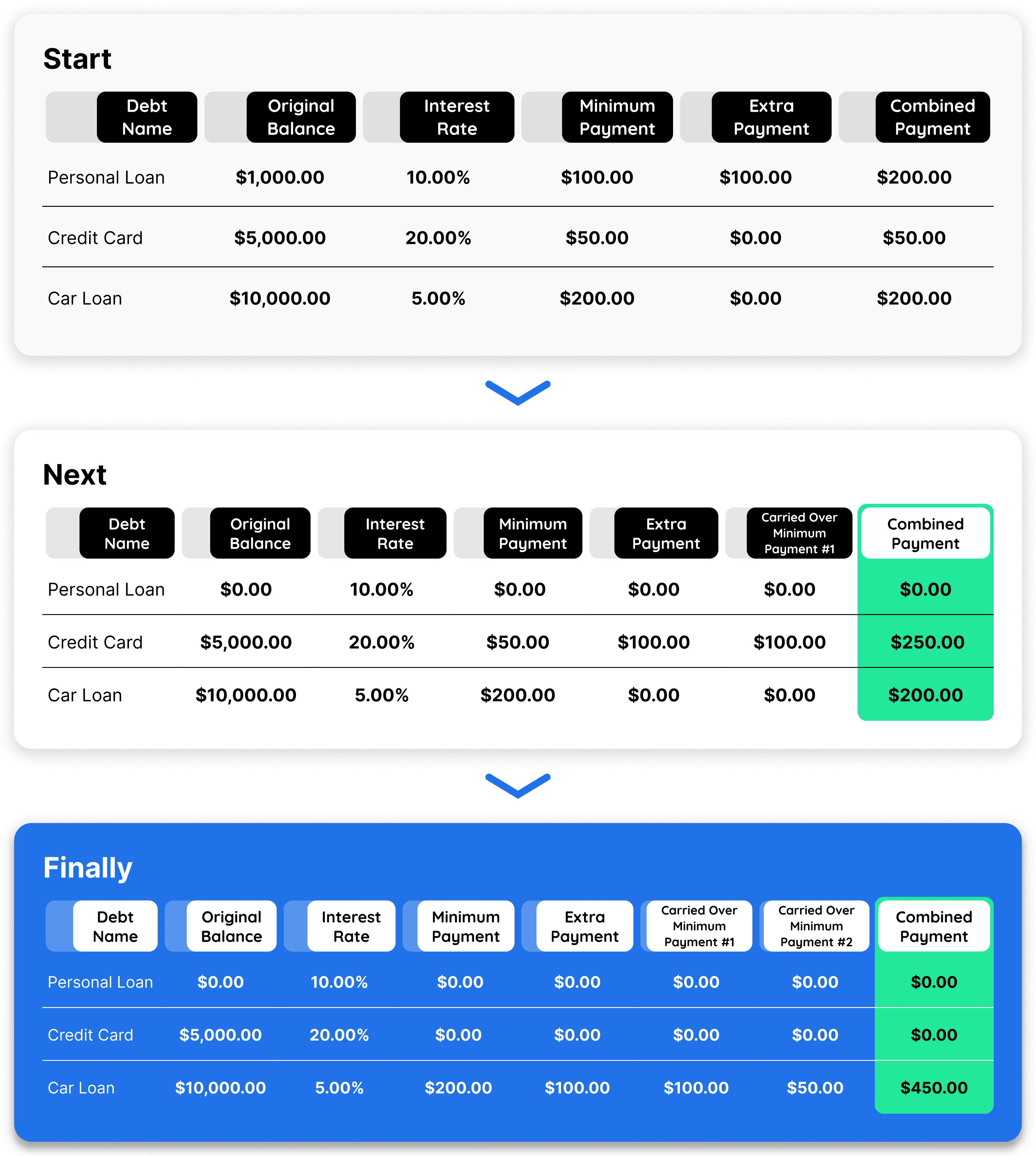

Snowball method

With the Snowball Method, we will prioritize the debt with the smallest balance first.

We will add our extra snowball to the first debt’s minimum balance and continue the extra payment until debt number one is completely paid off.

Once debt number one is cleared, we take the amount we were paying as a minimum payment for our first debt, along with the extra snowball, and now apply it to our second debt. By adding both the snowball and the first minimum payment to our second debt, we speed up the momentum of our debt paydown without affecting our monthly budget.

We continue until we have paid off all our debts (adding your mortgage to this process is optional).

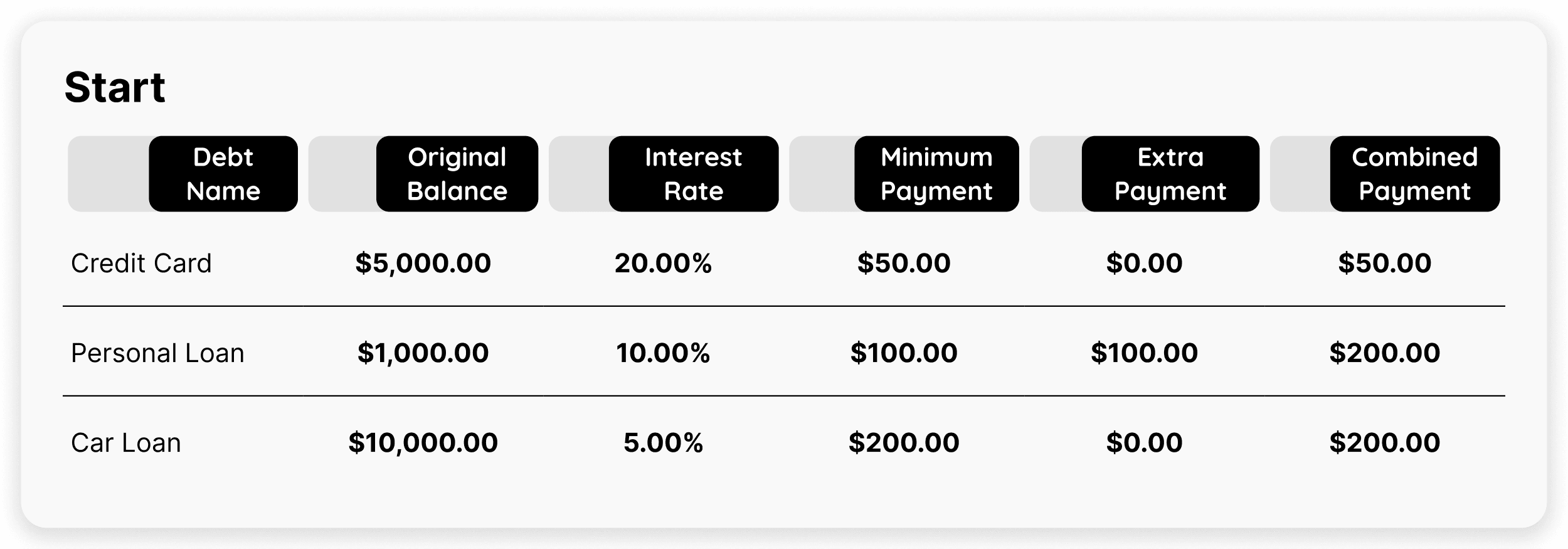

Avalanche method

The Avalanche Method follows the same steps, except that we will prioritize the debt with the highest interest rates first.

Which is better for you? It depends.

The avalanche method makes more sense mathematically since paying down the principal on high-interest-rate debts reduces the amount you will owe over time.

The advantage of the snowball method is psychological. Changing habits and taking on the goal of paying down debts you may have accumulated over the years can be hard. Getting some early wins by having one less thing to worry about can keep you motivated to tackle bigger hurdles.

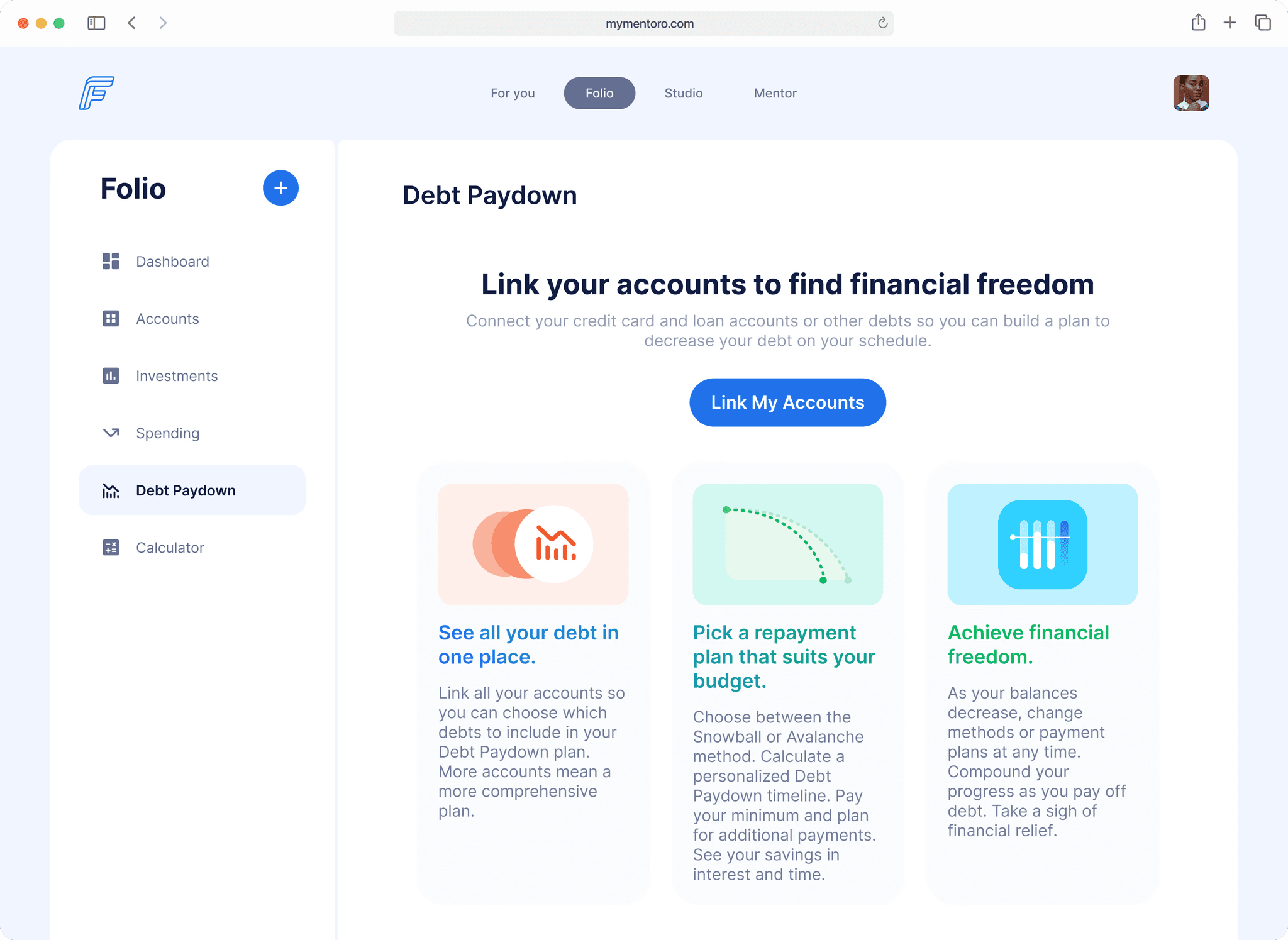

You've got tools to help you

Not sure which way to go? Folio has a Debt Paydown feature that allows you to connect your accounts and game plan each scenario. Since your balances are updated daily, it tracks your progress in real time.

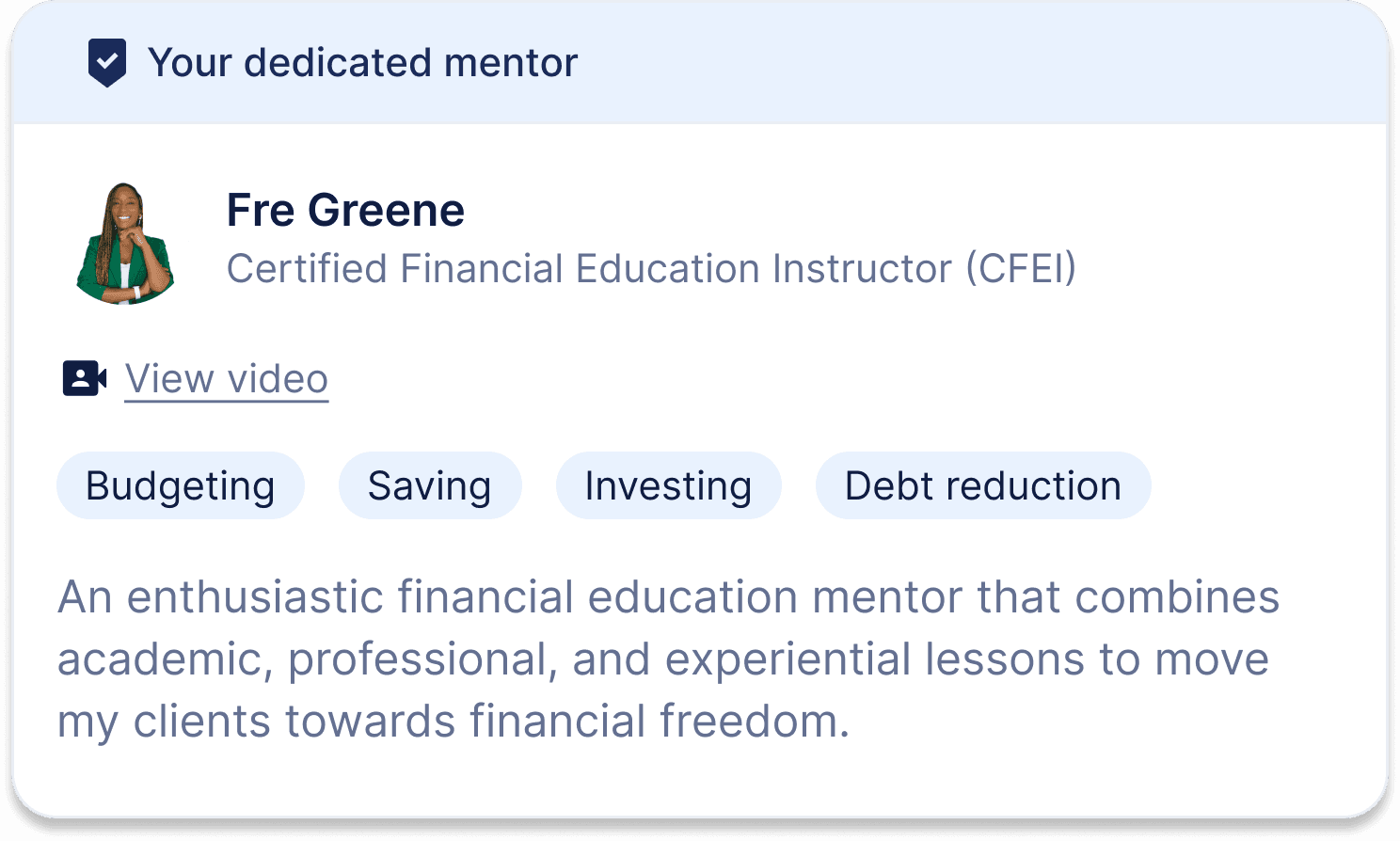

Need someone to talk it through with you? Fruition gives you access to Mentors like Fre Greene who can walk you through the process and help you stay on track with one-on-one meetings.

Becoming debt-free is a powerful step in improving financial wellness. It gives you flexibility to pursue other goals and reduces stress. We’re here to help you every step of the way.